CRM for Community Banks: a Game-Changer in the Digital Age

Editor’s note: Natallia shares how community banks can leverage customer relationship management (CRM) technology and strategic innovation to strengthen customer engagement, enhance lending services, and compete effectively with both fintech disruptors and financial giants.

Community banks have long distinguished themselves as local financial providers with a deep understanding of their customers' needs. However, this advantage is no longer exclusive to them, as nationwide banks leverage their vast resources to enhance customer relationship management through innovation. In an increasingly competitive landscape, community banks must go beyond proximity and personal relationships to maintain their edge.

Tightening Competition With Megabanks Puts Community Banks at Risk

Known for their personalized, customer-first approach, community banks have historically been the financial backbone of U.S. counties. However, decades of industry consolidation and the dominance of megabanks — institutions with assets exceeding $100 billion — have placed smaller banks in a precarious position.

In 1995, megabanks held only 17% of all banking assets, but by 2022, their market share had surged to more than 70%. Meanwhile, community banks have seen their share plummet from over 30% to less than 15% throughout the decade. Although 97% of banks making up the U.S. banking system are community banks, the 10 largest U.S. banks today account for nearly 53% of total assets. To put this in perspective, the assets of the U.S. largest bank — JPMorgan Chase — now surpass those of all U.S. community banks combined. This increasingly competitive environment makes both customer acquisition and retention more challenging for smaller financial institutions.

Bigger banks are becoming more customer-oriented — with the help of technology

While community banks maintain a physical presence close to their customers, megabanks are rapidly closing the gap by investing heavily in technology that replicates the personalized service traditionally associated with local institutions.

Leading financial giants are integrating high-tech banking software to enhance marketing, sales, customer support, and the entire customer lifecycle. For instance, JPMorgan Chase has partnered with over 100 fintech firms to develop innovative banking solutions. Other major players, including Wells Fargo, Bank of America, Citigroup, Goldman Sachs, and Morgan Stanley, are following a similar path, prioritizing fintech collaborations to improve customer engagement.

To safeguard their market share, community banks must rethink their business strategies, leveraging their strengths and incorporating digital advancements to maintain a customer-first approach.

Why community banks must enhance their customer-centric approach

Building a strong customer-focused strategy is no easy task, and simply being a local institution is no longer enough. It’s unrealistic to assume that a community bank inherently understands its customers better than larger financial players who leverage advanced technology. Without keeping pace with innovations and adopting data-driven strategies, community banks will struggle to compete in a landscape where personalization is increasingly powered by technology.

In comparison to the sophisticated data-driven strategies of megabanks, community banks may find themselves relying on informed guesswork rather than precise customer intelligence. Instead of assuming they have superior knowledge of their customers, they should critically assess their capabilities by asking:

- Do we have comprehensive statistical data for multi-dimensional customer analysis?

- Do we understand our customers’ behavior in terms of channel usage and product preferences?

- Are we tailoring financial products and services based on these insights?

The Shifting Lending Landscape: A Growing Challenge for Community Banks

For decades, community banks have relied heavily on interest-based revenue from loans, primarily offering small business financing and mortgages to local residents. As stated in the National Survey of Community Banks, small business lending and mortgages for county citizens have been the most prominent lending activities of community banks. However, new players are now aggressively entering this space, threatening what was once a stronghold of community banking.

Lending competition is at full blast

1. Online lenders

Since the first online lender emerged in 1985, digital platforms have been reshaping customer expectations by making loan applications faster and more accessible.

For example, Quicken Loans, specializing in mortgages and refinancing services, markets its service with the simple yet powerful slogan: “Push button – get mortgage.” The New York Times even dubbed it “the new mortgage machine,” and J.D. Power, in their “Primary Mortgage Origination Satisfaction” study, ranked Quicken Loans highest in customer satisfaction for mortgage origination for seven consecutive years.

Square is another successful online lender that focuses primarily on small business loans. The company issued more than $2.3 billion in financing to businesses through its Square Capital program in 2019 alone and processed 76,000 SBA PPP loans totaling $820 million in six weeks amidst the Covid-19 pandemic burst.

2. Banks and financial giants

While fintech companies dominate the alternative lending space, major banks and financial institutions are also expanding their digital lending services.

For example, Wells Fargo launched FastFlex, an online loan tool designed specifically for small businesses. With real-time approvals, businesses can access loan amounts ranging from $10,000 to $35,000, often as soon as the next business day. The platform’s competitive rates and streamlined process make it a compelling option for small business owners.

Similarly, American Express entered the small-business lending market with its Working Capital Terms platform. This service allows existing AmEx cardholders to secure loans within minutes, with funds deposited directly into vendor accounts. With low interest rates (as little as 1.5% for a 90-day loan), this solution offers an attractive alternative to traditional credit-based financing.

What’s at stake for community banks

With numerous alternative lending options emerging, the traditional lending model for community banks is under significant pressure. Both online lenders and financial giants are actively working to claim a larger share of the loan market by offering customers:

- Seamless digital platforms.

- Faster approval processes.

- Competitive interest rates.

- More personalized loan options through advanced data analytics.

If community banks fail to adapt to this evolving landscape, they risk losing ground to more technologically advanced competitors. Continuing to rely on outdated communication methods, such as snail mail for customer outreach, is no longer sustainable.

Since loans remain the lifeblood of most community banks, they must innovate. This could mean focusing on niche lending opportunities — such as construction or startup loans — or accelerating loan portfolio growth by investing in the right technological tools to enhance efficiency and customer experience.

Why Community Banks Need CRM

A banking CRM can help community banks deepen their understanding of customers by consolidating all collected insights into a single, easily accessible platform. With a centralized database, bank staff can retrieve a complete customer profile, including personal preferences and recent transactions, ensuring that every interaction is relevant and data-driven. Since human memory is fallible, a CRM also helps establish systematic and timely communication, allowing banks to better nurture customer relationships.

By implementing a banking CRM system, community banks can improve core functions such as communication, cross-selling, and financial advising within their local communities. For example, Union National Community Bank, a Pennsylvania-based institution with a 150-year-long history, achieved $1 million in efficiency gains, increased its revenue, and prevented customer churn thanks to tailored CRM technology. However, given the limited budgets of community banks, selecting the right CRM functionality is a critical challenge.

Basic CRM features

To make CRM implementation cost-effective, community banks should prioritize core features that deliver immediate value. Many of these capabilities come as standard in most market-available CRM solutions and require minimal customization. While a banking CRM offers extensive functionality, smaller institutions should focus on essentials to avoid underutilization and overspending.

At the initial stage, community banks should adopt fundamental features such as:

- Customer profiling – creating comprehensive customer records for personalized service.

- Mass marketing communication – streamlining outreach efforts via email, phone, or text.

- Basic sales workflows – automating routine sales and service processes.

Once these features are successfully integrated, banks can consider expanding their CRM capabilities with more advanced tools.

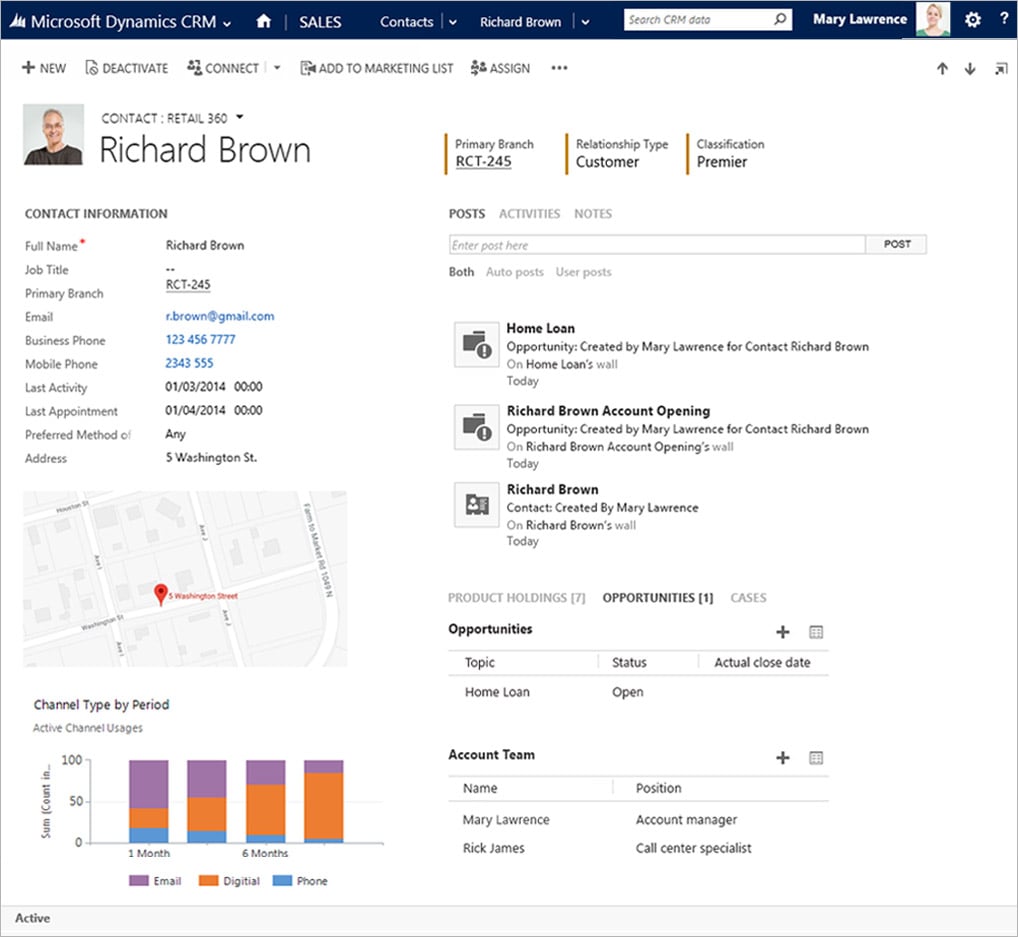

Sample interface of a banking CRM system by ScienceSoft

Advanced CRM features

Advanced CRM functionality can add significant value to a community bank, but every investment must be carefully assessed for its return on investment (ROI). Studies by Nucleus Research showcase that advanced banking CRMs can yield an ROI of $8.70 for every dollar spent. However, each bank should evaluate its own strategic priorities before investing in additional features.

With guidance from CRM consultants, community banks can tailor their solutions to include:

- Customer segmentation – categorizing customers based on demographics and financial behavior.

- Personalized marketing automation – delivering targeted promotions based on customer data.

- Custom workflows for cross-sales and retention – enhancing engagement strategies to increase customer lifetime value.

Using CRM to enhance loan offerings

A banking CRM is traditionally used to manage customer relationships, but it also plays a crucial role in optimizing a bank’s loan portfolio. By consolidating customer data into a single platform, CRM enables banks to perform key tasks such as targeted marketing, lead management, and loan analytics.

When properly configured, a CRM can provide the following loan-related benefits:

- Segmentation – identifying high-potential borrowers based on demographic and financial criteria, allowing banks to match customers with the right loan products.

- Targeting – using in-depth customer data to personalize loan offers via email, phone, or promotional campaigns.

- Follow-up automation – integrating CRM with email systems to assign leads to loan officers, ensuring timely communication and improved conversion rates.

- Loan analytics – tracking loan performance, forecasting deal closures, and identifying areas for improvement in loan campaigns.

By leveraging CRM technology, community banks can ensure that potential leads are not overlooked while also avoiding excessive or irrelevant outreach. A well-implemented CRM helps banks craft effective loan marketing strategies, track high-value customers, and drive loan portfolio growth.

The Bottom Line

Community banks hold a unique advantage over larger financial institutions: agility. Unlike megabanks, which often struggle with legacy infrastructure, siloed data, and bureaucratic inefficiencies, community banks can adapt more quickly and foster seamless collaboration between departments. By reinforcing these strengths with CRM technology, they can enhance customer acquisition and retention and deliver first-class service while staying true to their local, relationship-driven roots.

Whether the goal is to elevate customer experience, streamline operations, or safeguard lending portfolios against growing competition from fintechs and megabanks, CRM is a strategic solution. With the widening range of CRM platforms, rolling out a tailored CRM is no longer a matter of exorbitant expenses for community banks. In ScienceSoft’s recent projects, we managed to deliver platform-based CRM systems for smaller financial institutions within the $50,000–$150,000 threshold.