Still Budgeting Health Insurance in Spreadsheets? Here's a More Effective Tech Stack

Editor's note: Olga Vinichuk, Insurance IT Consultant at ScienceSoft, proposes automation and analytical tools for health insurance budgeting and shares how to optimize costs and boost user adoption for them. The interview is led by Stacy Dubovik, a financial technology researcher.

Spreadsheets Can't Sustain Health Payers' Budgeting Anymore. Alternatives?

SD (Stacy Dubovik): Good old spreadsheets have been a staple in health insurance budgeting for decades. Are they still feasible in 2025?

OV (Olga Vinichuk): There's much more data in health insurance today than twenty years ago. Payers can now use dozens of data points, from member credit scores to ACA rules, for financial forecasts. If you want to keep dealing with budgeting and forecasting in spreadsheets, it means somebody has to manually assemble, clean, and update massive datasets from multiple sources. It is becoming unsustainable.

Here's how I would summarize the most pressing issues my clients are facing with spreadsheets:

- Short-term forecasting is inefficient and error-prone. Let's take loss reserve budgeting. You're not just tallying what has already been paid; you're projecting costs based on historical claims and external factors like Medicare fee schedules, regional demographics, and reinsurance fees. For short-term sensing, you could include dynamic data like the insureds' behaviors, pharma pricing, and disease stats. Manually preprocessing this disparate data each time you need to adjust your projections is a nightmare in terms of time and effort. What's worse, a single human error could cascade into hundreds of thousands in losses due to misallocation.

- Spreadsheets do not support complex multi-dimensional analytics. Even if you obtain data on variables like claim seasonality, demographic shifts, or medical provider cost variations, your heritage tool won't be able to process them all simultaneously.

- Delayed data access complicates decision-making. In a spreadsheet system, when one group updates their assumptions, say, the actuarial team projects higher costs for a new flu treatment program, the finance team has to sync that to their budgeting workbook manually. Those lags in data sharing may lead to delayed and misaligned decisions.

- Weak data security compromises regulatory compliance. With spreadsheets' basic access controls, it's difficult to ensure that only authorized parties can view and modify specific budgeting data. Meanwhile, the underwriting and claim data used for financial forecasts might contain PHI. Storing such data in spreadsheets and emailing the docs between teams exposes the data to breaches and accidental disclosures penalized by HIPAA.

SD: Then, what alternative solution do you propose? Are there any specific requirements for an efficient budgeting system?

OV: Naturally, a better budgeting system must address all the shortcomings of spreadsheets.

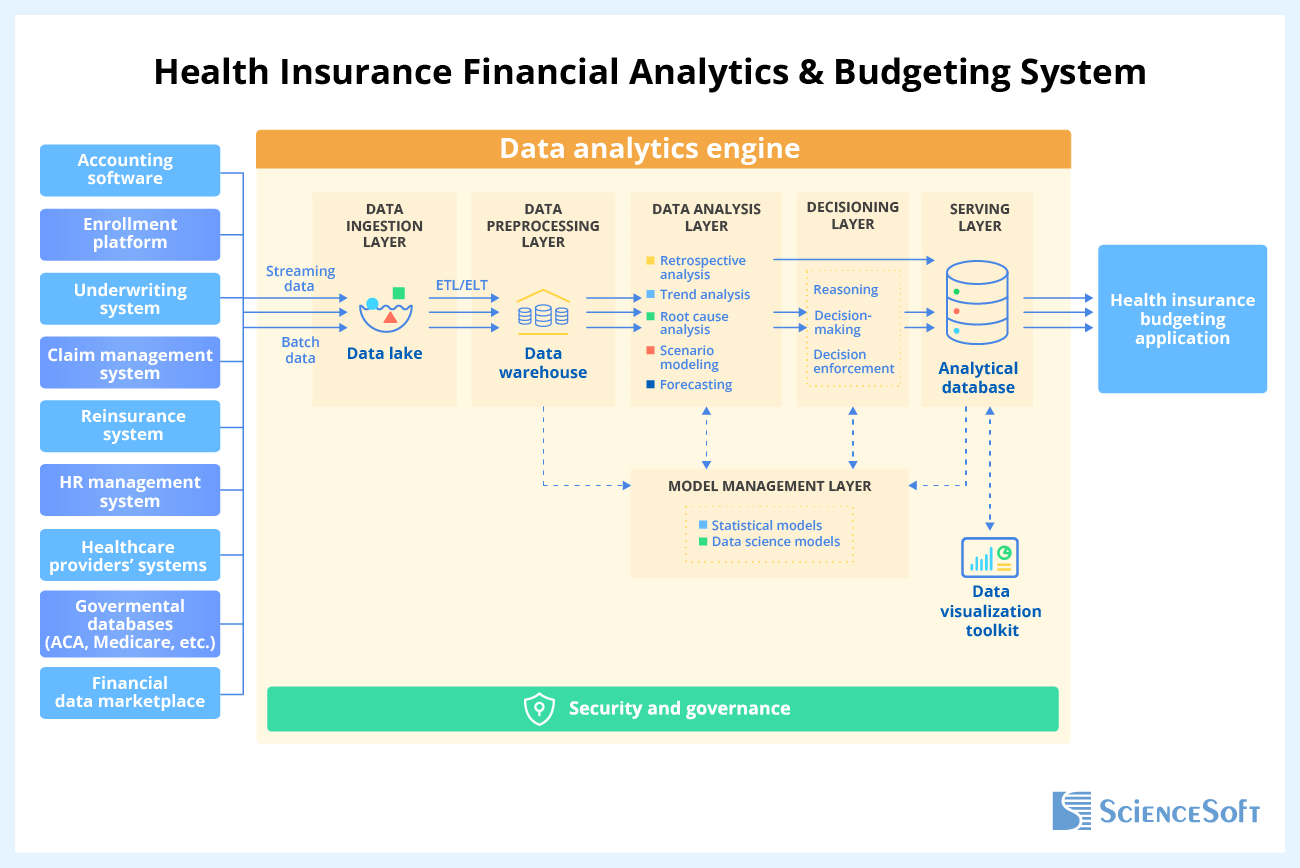

First and foremost, your solution should be integrated with the systems that host your budgeting data feeds, including your corporate software (accounting system, enrollment platform, claims processing solution, etc.) and external data sources like healthcare provider systems, pharmacy benefit management systems, and public health databases. This means the tool has to be equipped with APIs and connectors to interact with versatile systems.

Secondly, the data processing pipeline should be maximally automated to deliver the speed and efficiency necessary for agile forecasting. For this, make sure your software supports multiple health insurance data formats and includes functionality for automated data capture, data conversion to the structured format, real-time analytics, and reporting in your preferred form. Straight-through validation of the obtained data is crucial to preventing errors in your financial projections.

Sample architecture of health insurance financial analytics & budgeting systems by ScienceSoft

Multi-dimensional modeling and forecasting engines are another must for accurate budgeting in complex scenarios like responding to loss reserve utilization increases or introducing behavior-based health policies in select regions. Let's say you want to determine how an increase in high-cost claims, driven by the rising specialty drug use, affects your claim reserves. The tool should allow you to input variables like regional drug utilization trends, provider contract terms, and member demographics and configure different scenarios (e.g., changes in formulary coverage or stop-loss thresholds). It should automatically calculate multiple reserve metrics, such as claim payouts, reserve thresholds, and required funding amounts. Add tailored graphs and side-by-side views to make the forecasts and data points easy to review and compare.

For high-precision external risk forecasts, the solution must be able to run Monte Carlo simulations and stress tests on predictive inputs like macroeconomic factors, CDC health trends, and regulatory updates. For instance, this would let you model economic downturn scenarios, anticipate how deferred medical care could reduce near-term claims but increase future chronic care costs, and factor these in your loss and contingency reserves.

Your solution must support continuous budget monitoring to give you a live view of budget utilization, variance, financial performance, and risk metrics. An essential feature to look for here is automated ACA compliance controls. The solution should track Medical Loss Ratio (MLR) limits in real-time and alert the responsible parties if administrative spending rises to a level that risks breaching the ACA's requirements. You'll need dedicated analytics to quickly simulate adjustments like reallocating funds or reducing side expenses to keep your ratios within the prescribed limits.

Seek robust security features to safeguard the budgeting solution and the sensitive data it stores. Role-based and row-level access controls, data encryption, MFA, and end-to-end audit trails are what you should expect at the baseline. However, in health insurance specifically, I always advise my clients to look for solutions that are explicitly built for HIPAA compliance (or equivalent regulations) — such software would already include all the essential security controls.

Mobile access to budgeting dashboards would enable leadership to track financial performance trends and approve budget adjustments on the go. Some of my health insurance clients stress that this is critical when dealing with rapid shifts like healthcare provider disputes or sudden demand and cost anomalies during open enrollment.

SD: What operational and financial outcomes can a health payer expect from a new budgeting solution like that?

OV: First of all, expect a significant lift in budget management speed. From my experience, automated financial data collection and consolidation alone can bring 65–80% time savings across the budgeting cycle.

For example, automated MLR calculations and compliance checks can save hours per day during peak reporting periods. Some of my clients who adopted specialized tools achieved a 40–80%+ improvement in the productivity of their budgeting teams.

Another critical outcome is streamlined cross-departmental collaboration. With a centralized system, your finance, actuarial, provider contracting, and compliance management teams will work from the same source of truth. They will have real-time visibility into the planned vs. actual budget and be able to easily coordinate.

Ultimately, quick data aggregation and robust financial forecasting will allow you to react to changes faster. For example, suppose a direct competitor introduces an aggressively priced high-deductible health plan. Your actuaries can rapidly project their impact on your enrollment and margin, simulate coverage term adjustments, and enforce them before losing revenue.

SD: And yet, it looks like the majority of health insurers still haven't abandoned their spreadsheets. Why so?

OV: Indeed, over 80% of health insurers still use spreadsheets for strategic budgeting.

When I ask my clients in the domain about the reasons, they commonly cite potential risks of technological errors, project failure, and low user adoption among the main barriers. However, my experience with a few recent projects at ScienceSoft proves that there are workable cures for all of these risks. There are best practices and technologies for preventing errors in financial software. As for project success, it is usually measured by the impact on the entire company's operations and bottom line, which means it must also be planned in the same way. Your budgeting initiative should not be a standalone project but a logical part of a broader digital transformation strategy.

Things are trickier when it comes to adoption. I believe employee resistance to change remains the top reason why insurers are still using spreadsheets in 2025. Financial clerks are infamous for loving their established routines and old-school tools, so they will be suspicious of any new app you try to roll out. I believe human connection would work better than any UX trick here. Simply put, pilot the app on a small group of less resistant financial team members first and let them spread the word and share their experience with their colleagues.

Bringing Modern Budgeting Software to Health Insurance: Ways to Cut Investments and Boost Adoption

SD: Let's talk implementation. Are there any ready-made health insurance budgeting tools on the market that you can recommend?

OV: Off-the-shelf suites like Workday Adaptive Planning, Anaplan, and Jedox offer prebuilt multi-dimensional financial analytics and budget management capabilities. These tools come with customizable automation and AI-supported features designed explicitly for insurance businesses. They provide go-to APIs for integrating with popular commercial tools.

However, all three fall short in budgeting functionality specific to health insurance. For example, they do not come preconfigured to handle MLR reporting, ACA compliance controls, forecasting for high deductible health plans, and cost-based member tracking. You would require extensive efforts and investments to tailor these OOTB products to your workflows. Connecting them to your corporate systems can be time-consuming and costly as well.

Custom software incurs higher upfront costs but offers more advantages. A custom health insurance budgeting solution can be designed with your business specifics in mind and easily adapted to your evolving needs in the future. From my experience, the option is particularly rewarding if you need integrations with legacy internal systems or require compliance with local regulatory standards. Also, custom software is the safest choice for AI-supported budgeting automation.

Custom development may seem like a huge investment, especially when it comes to customized AI components. However, there are proven ways to optimize project time and costs. My colleagues at ScienceSoft have recently compiled an overview of cost reduction practices we apply in our projects — check a dedicated page for deeper insights. In my practice, a custom solution for health insurance budgeting can be built for $200,000–$400,000.

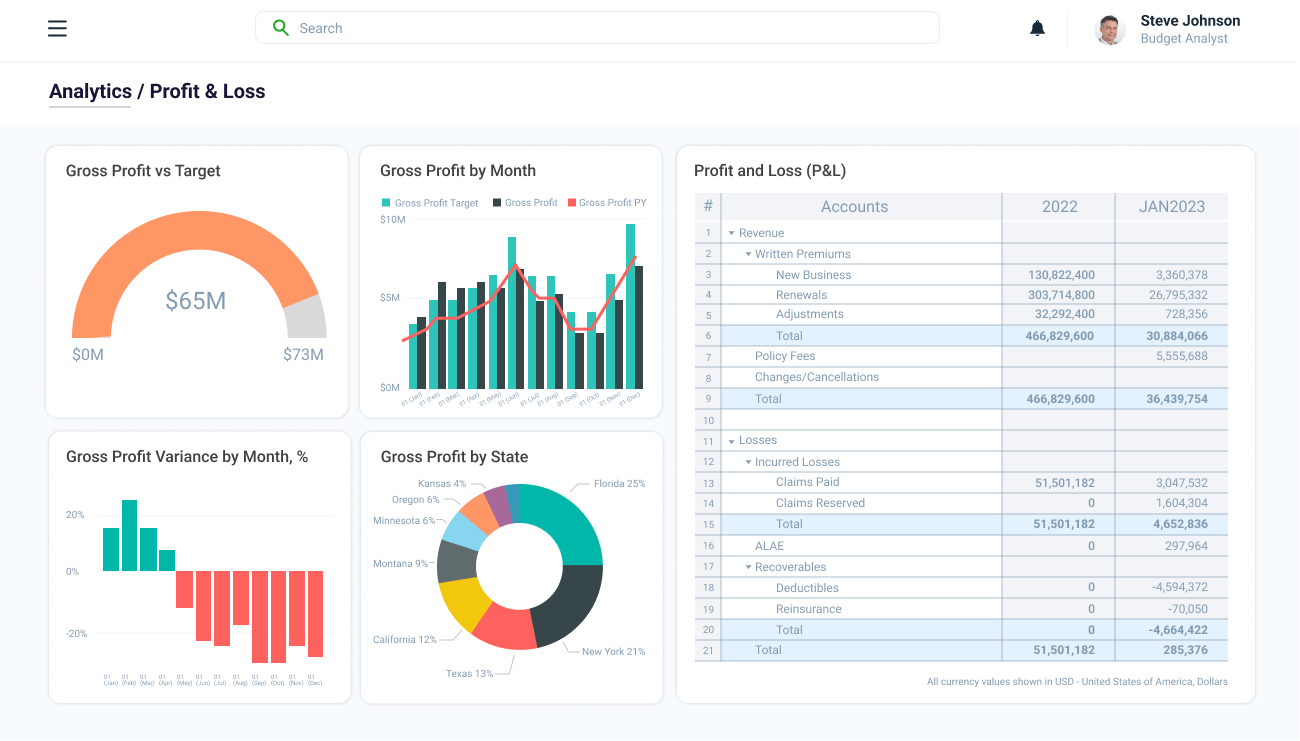

Sample interfaces of health insurance budgeting applications by ScienceSoft

SD: Returning to user adoption, which, you said, is a critical success factor for budgeting transformation. How could health insurers foster high adoption of their new budgeting solutions?

OV: First, involve end users — your finance teams, actuaries, and department leads — at early software planning stages and give employees a voice in defining functional requirements for the future solution. Incorporating employee input ensures that the planned features reflect the teams' actual needs and helps prevent user frustration.

Prioritize features that deliver immediate improvements in daily budgeting routines. Your MVP should focus on automating the most labor-intensive tasks and delivering critical financial insights faster than existing tools. When employees see instant improvements in efficiency, say, hours saved due to automated data entry or simplified multi-scenario analysis, they are far more likely to buy in. This approach creates a strong foundation of trust in new technology and encourages teams to embrace the new tool as an indispensable part of their workflows. Establishing feedback loops and actively gathering employee opinions post-launch will let you quickly refine and evolve your budgeting solution.

In terms of adoption, the usability of your budgeting system is just as important as its functionality. Prioritize straightforward user journeys to minimize redundant actions and ensure prompt user access to the required data. Configuring model parameters, setting budget targets, and reforecasting costs should be as simple as clicking dropdowns or adjusting sliders. From my experience, familiar interfaces are a crucial adoption driver. In ScienceSoft’s projects, we usually retain Excel-like data visualization options and UI elements so that employees feel comfortable navigating the system from day one.

Employee training is another cornerstone of adoption. Provide in-person or remote scenario-based sessions to show how the new system handles everyday budgeting tasks and help your teams master the new solution quicker. Consider holding workshops tailored to specific roles, for example, financial planners and regulatory compliance teams, to ensure employees feel confident applying the tool to their unique responsibilities.

User support is a must, especially during the early post-launch period when your budgeting teams navigate the unfamiliar system and may struggle to resolve issues themselves. In the early stages, frustration can quickly mount and hamper adoption. A human hand here is crucial not only for comprehensive technical guidance but also for psychological reassurance.

If you need advice on budgeting software implementation strategies for your specific case, feel free to contact me or other consultants at ScienceSoft.

Read part two of the interview where ScienceSoft's Olga Vinichuk goes into detail about using artificial intelligence (AI) for accurate and efficient financial planning in health insurance.