Large Language Models (LLMs) for Insurance

Features, Architecture, Techs, Costs

ScienceSoft combines 36 years of experience in artificial intelligence with 13 years in insurance software engineering to deliver tailored insurance automation solutions powered by market-leading large language models.

for Insurance - ScienceSoft")

Key Opportunities of Large Language Models for Insurance

Large language models for insurance are designed to automatically capture, consolidate, classify, and summarize massive volumes of heterogeneous insurance data, making it easier to derive accurate insights for decision-making across the insurance value chain.

LLM-enabled automation lets insurers process underwriting and claim documents more than 50x faster, which enables more than 4x quicker quote submissions and claim responses. Using LLMs for policy and report checks brings up to a 400% increase in review capacity while ensuring 95%+ accuracy of gap detection.

LLM-based virtual assistants can understand complex natural language prompts and instantly respond to insurance professionals in a human-like manner. By powering their support chatbots with LLMs, insurers get 70%+ of customer inquiries handled automatically in real time. This drives, on average, a 7% increase in client satisfaction (CSAT) and can reduce agent workload by up to 50%.

LLMs in Insurance: Market Info and Value Considerations

The global market for generative AI in insurance is anticipated to reach $14.4 billion by 2032, growing at a CAGR of 34.4%. Considered a subclass of generative AI algorithms, large language models are rapidly gaining popularity among insurers worldwide due to their ability to handle time- and effort-consuming data processing tasks.

For insurance professionals, who spend up to one-third of their time aggregating information, LLMs' ability to instantly consolidate multi-source data and adapt it for human perception offers a solution to one of the biggest operational hurdles in insurance. MunichRe, the world's largest reinsurer who is already investing in LLM pilots for life and disability lines, believes that if properly trained, tested, and controlled, LLMs can bring immense value for underwriting and claims.

Deloitte stresses that insurance-specific focus on "vertical" use cases (i.e., disparate functional areas requiring in-depth domain expertise) may hinder quick LLM adoption in the field. Applying LLMs effectively across specialized insurance functions would require tuning general-purpose language models, training them on a specific discipline, or building dedicated LLM algorithms.

How LLMs for Insurance Work

Main use cases

![]()

Customer onboarding

LLMs can automatically capture customer data from textual and voice applications and pull out KYC-relevant details from insureds' documents for faster pre-qualification.

![]()

LLMs can auto-consolidate risk data from customer documents and third-party sources and summarize data on apparent and potential perils that may affect written premiums.

![]()

LLMs can auto-extract claim insights from FNOLs, policies, and multi-format loss evidence documents and compose claim summaries to inform settlement decisions.

![]()

LLMs can instantly recognize insurance document inconsistencies that may indicate customer or employee fraud and flag them for a closer investigation by human experts.

![]()

Compliance

LLMs can auto-verify document compliance against an insurer's internal rules and legal guidelines. They can also screen regulatory changes (e.g., NAIC, NICB, IFRS, IA standards) and report new clauses.

![]()

Customer service and support

LLM-based assistants can understand the nuances of client inquiries, give relevant real-time responses, and recap customer calls and chats for human agents.

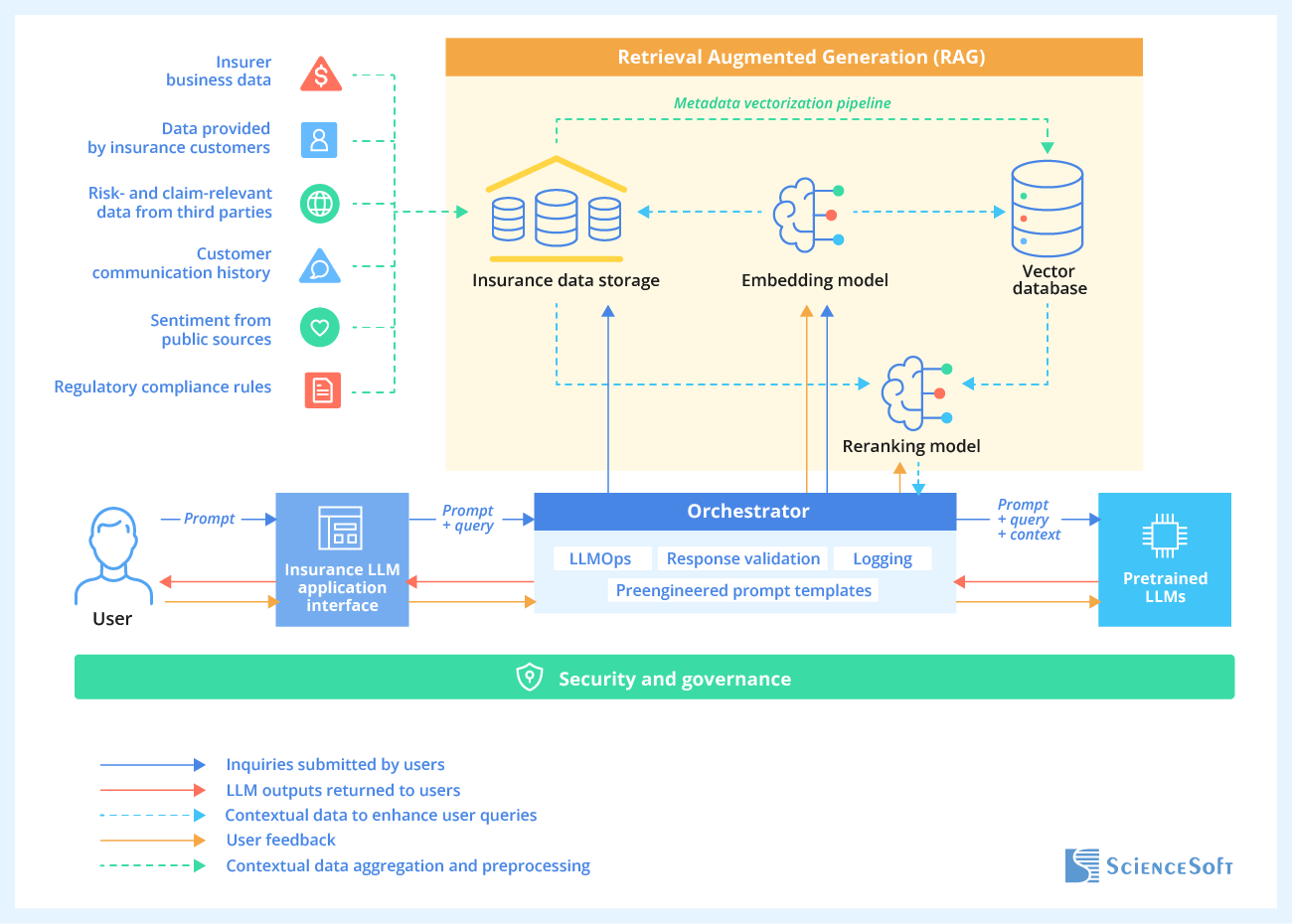

LLM solution architecture

ScienceSoft uses pretrained LLMs (GPT-4, LLaMA, Claude, etc.) as a core building block of LLM solutions for insurance. We employ enhancement techniques like prompt engineering, parameter-efficient fine-tuning (PEFT), and retrieval augmented generation (RAG) to augment LLMs with specialized insurance knowledge and business data in a fast and cost-effective way.

Below, ScienceSoft's solution architects share a sample architecture of RAG-enabled insurance LLM solutions we deliver and describe its key components and data processing flows:

- Using an LLM-supported application, an insurance professional or a customer asks a question or formulates a task. The app can be built on top of insurer software, as a standalone web or mobile solution, or as an in-browser tool.

- The LLM app instantly routes the user's prompt to the orchestrator. The orchestrator connects the client-side app, LLMs, and LLM enhancement components and relies on the Large Language Model Operations (LLMOps) framework to ensure effective real-time communication and smooth data transition between the system parts.

- The orchestrator queries the insurer's data storage to provide prompt-relevant structured data (risk score, policy date, claim type, etc.) and the RAG embedding model — to retrieve unstructured contextual data like claim documents, customer conversation histories, and compliance instructions. For efficient semantic search, unstructured data in the form of PDFs, digital images, web pages, etc., needs to be presented in a vector form. To achieve this, ScienceSoft sets up a vectorization pipeline for automated insurance metadata cleansing, chunking, and conversion to vectors. The vectorized data is stored in a vector database.

- The ranked results of the hybrid search (plain text, numerical, and vector) are merged, scored, and composed into an optimal result set using a tailored reranking model. The model routes a single search response to the orchestrator.

- LLM-ready prompt templates with custom logic for applying contextual data ensure accurate auto-filing of insurance-specific prompts and help stay within the predetermined prompt length limits. The orchestrator pulls out the case-fitting template, triggers template filing, and sends the enhanced prompt to the chosen pretrained LLM.

- The pretrained LLM processes the prompt and returns the response to the user. Depending on the client's needs, ScienceSoft can involve a closed-source LLM (e.g., by OpenAI, Anthropic, Meta), an open-source LLM (by Hugging Face, Replicate, etc.), or integrate with large cloud providers' services like Amazon Bedrock or Azure OpenAI Service, which grant access to several market-leading models. Our engineers incorporate LLM event logging and response validation at the orchestration layer to enable more control over solution performance and LLM output quality.

- The user gives feedback on the response's accuracy and relevance. The feedback informs further LLM fine-tuning, e.g., via reinforcement learning with user feedback.

Key capabilities of LLMs for insurance

![]()

Prompt-based interaction

The insurer’s employees (agents, underwriters, actuaries, claim specialists, etc.) and insureds interact with LLM-based digital assistants using textual prompts. LLM copilots apply advanced natural language understanding and inference "skills" to support real-time conversations.

![]()

Call transcription and voice synthesis

VoIP calls get auto-transcribed and summarized for further use by insurance employees. Multimodal LLMs support stream voice recognition and help classify real-time calls by category (e.g., policies, claims, reports), which lets insurers route the inquiries to the appropriate team quickly. Advanced solutions use voice synthesis to automate spoken responses.

![]()

Contextual data capture from the insurer's data storage

LLMs themselves cannot access insurers' proprietary data. Integrating the LLM app with the insurer's centralized data storage lets the models capture real-time contextual data obtained from corporate systems (an insurance portal, CRM, etc.) and connected third-party sources (e.g., tracking systems of business clients, record systems of healthcare partners, public registries).

![]()

Data extraction from documents

An LLM system automatically extracts textual data from documents provided by customers, brokers, agents, and external stakeholders. Documents can be related to eligibility for insurance services (IDs, salary slips, utility bills, business licenses), risks (loss run reports, asset passports, safety policies, environmental impact reports), claims (FNOLs, incident reports, witness statements), and more.

![]()

Insurance data summarization and export

The extracted data can be summarized according to predefined rules or real-time prompts, put into chosen document templates (e.g., underwriting forms, loss adjustment forms, quote templates), and exported to the connected systems handling their respective workflows: risk assessment, policy pricing, parametric payouts, accounting, etc.

![]()

Third-party data validation

LLMs recognize data patterns inherent to various insurance documents and automatically spot missing and controversial inputs in the documentation. Discrepancies are instantly communicated to the responsible parties to trigger a manual review.

![]()

Insurance document review

LLMs extract sensitive sections of insurance policies, invoices, disclosure reports, etc. and present them to the responsible reviewers, who further vet the data for accuracy and compliance. LLMs can be instructed to compare document drafts against standardized templates and case-specific hard facts and notify insurers of document gaps.

![]()

Insurance knowledge consolidation

In response to insurer queries, LLMs categorize the obtained insurance data by service area, policy type, customer segment, etc., assemble it into employee handbooks and educational materials, and route the produced documents to the insurer's corporate knowledge base to be available for employee guidance, training, and self-learning.

Breaking down a misconception about LLMs and agentic AI

While LLMs are great at unstructured data synthesis and NLP, they cannot, on their own, automate complex insurance tasks like risk monitoring, dynamic premium recalculation, or fraud response. To automate these tasks, you need to combine multi-faceted LLMs with reinforcement learning algorithms strong at numerical reasoning and predictive decision-making, and integrate the models with your process automation tools. The resulting solution is an AI agent system, and is what you need for truly autonomous digital workflows.

See How LLM-Based AI Agents Transform Insurance Claims

Watch how ScienceSoft’s custom AI agent automates conversational claim verification and fraud insight generation for investigators. Built on AWS Bedrock AgentCore and powered by OpenAI’s leading LLMs, the solution boosts investigator capacity by over 40% and drives 20%+ higher fraud detection rates through additional, sentiment-based fraud indicators.

How Insurance Market Leaders Benefit From LLM Solutions

![]()

Markel Uses LLMs to Boost Underwriter Productivity by 100%+

Markel Group Inc., a US specialty insurer with over 90 years in business and $16B+ in annual revenue, relies on an LLM-fuelled risk management platform by Cytora to automate pre-underwriting activities. The solution extracts and summarizes risk information from broker submissions and external sources, triages risks in the context of Markel's underwriting strategy, and presents decision-ready risks to underwriters.

LLM-driven data processing automation helped Markel achieve a 113% increase in the underwriting team's productivity and reduce time-to-quote for commercial insurance clients from 24 hours to 2 hours.

![]()

Zurich Adopts LLMs to Review Claim Documents 58x Faster

Zurich Insurance Group, one of the world's largest multiline insurers with 55K employees and customers in 215 countries, turned to an LLM-based document mining platform by expert.ai to automate claim review. The solution leverages Zurich's business-specific knowledge graph to understand and automatically process the company's multi-format claim documents across general, life, and farmers' insurance.

By automating data extraction and summarization with the help of LLMs, Zurich managed to cut claim review time by 58x and save 8 hours of work time per policy review while achieving high data processing accuracy.

Techs and Tools We Use to Implement LLMs for Finance

Large language models

![]()

![]()

![]()

![]()

LLM platforms and services

![]()

![]()

![]()

![]()

![]()

![]()

Deep learning frameworks and libraries

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Orchestration

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Programming languages

![]()

Vector databases

![]()

![]()

![]()

![]()

![]()

![]()

LLM output validation

![]()

![]()

![]()

![]()

Big data processing

![]()

![]()

![]()

![]()

![]()

Challenges of LLMs for Insurance and How to Tackle Them

![]()

Challenge #1: Risks of inherited inaccuracy

Biased inferences, misinformation, and toxicity produced by pretrained LLMs may propagate to insurance LLM solutions, leading to erroneous responses, unintended discrimination, and potential breaches of ethical servicing guidelines.

Solution

![]()

Challenge #2: Lack of control over data security

Solution

Costs of Implementing an Insurance LLM Solution

From ScienceSoft's experience, the cost to implement an LLM solution for insurance may vary from $250,000 to $1,000,000+, depending on solution complexity, model enhancement approach, architectural and tech stack choices, and security and compliance requirements.

Here are our ballpark estimates for common scenarios:

![]()

$250,000–$350,000

An LLM-powered chatbot that handles client communication. RAG is applied to accommodate the insurance firm's specifics.

![]()

$300,000–$500,000+

An LLM assistant for insurance employees. The underlying LLMs are fine-tuned using PEFT and "upskilled" on specific insurance knowledge using RAG.

![]()

$1,000,000+

An LLM-based insurer copilot trained to reason on highly specific service aspects or new insurance models.

Insurance LLM Consulting and Implementation by ScienceSoft

In AI software development since 1989 and insurance IT since 2012, ScienceSoft provides comprehensive LLM services to help insurers and insurtech startups obtain effective LLM-powered solutions.

![]()

Insurance LLM consulting

We analyze the feasibility of LLMs for your business needs, advise on the cost-effective approach to LLM implementation, and provide security and compliance consulting. You receive the optimal feature set, architecture, and tech stack for your LLM solution, as well as the detailed project plan with cost and time estimates.

![]()

Insurance LLM implementation

Our team handles the project end-to-end, from pretrained model integration to LLM app design and coding. We establish secure LLM orchestration processes, enhance the model's insurance awareness via RAG and PEFT, and retrain an LLM in complex cases. You get an MVP of your insurance LLM solution in 1–4 months.

Our BFSI Clients on Their Experience With ScienceSoft

What stood out was ScienceSoft's proactive suggestions for cost-saving architecture design and tech stack solutions. Their input ensured we stayed within budget without compromising on software quality.

Partnering with ScienceSoft for our software maintenance and evolution initiative has been an excellent experience. Over the past 18 months, their team has transformed our underwriting platform into a well-oiled machine. <...> Their communication was exemplary; unlike our previous experiences with outsourcing, we never had to chase them for updates, and they were always prompt in responding to our queries.

Damien Sewell

Head of IT Projects

ScienceSoft’s quick buy-in and readiness to take the initiative made the project faster and less stressful for everyone involved, from Capital IM’s insurance specialists to leadership. We couldn’t have asked for a better IT partner.

Insights From ScienceSoft's Insurance IT Experts

Vadim Belski

Head of AI, Principal Architect, ScienceSoft

Fraud Detection AI Agents: 6 Guardrails for Insurers

Stacy Dubovik

Financial Technology and Blockchain Researcher, ScienceSoft

Interview

Using AI for Financial Planning in Health Insurance

Olga Vinichuk

Insurance IT Consultant and Lead Business Analyst, ScienceSoft

Technology overview

Bringing Smart Underwriting to Health Insurance

Featured Expert Talk

AI Agents for Insurance Claims Fraud Detection | Presentation at ITS 2025

Presentation by Vadim Belski, Head of AI and Principal Architect at ScienceSoft, from the 2025 Insurance Transformation Summit in Boston. Vadim explores the potential of agentic AI in insurance and demonstrates how claims AI agents can enhance fraud detection through conversational claim verification.